News and Insights

Ionic Technics inspects Global 7500

Ionic Technics, the aircraft technical services arm of Ionic Aviation, recently conducted the pre-financing inspection of a pre-owned Bombardier Global 7500 aircraft on behalf of an international lender.

The inspection was performed at short notice, and included a detailed physical inspection of the aircraft plus a review of the accompanying records. The findings from our review were supplied to our client in the form of a detailed inspection report.

With longstanding, all-round experience of both aircraft financing and technical services, Ionic Aviation has a unique understanding of the needs of those involved in the finance and leasing of not only private aircraft but commercial aircraft also.

We are therefore best placed to assist in your next project in the United Kingdom, mainland Europe or further afield.

Ionic Technics recently performing the pre-financing inspection of a beautiful Global 7500 aircraft.

Ionic Aviation to attend CJI Malta

Ionic Managing Director, Graeme Shanks, will be attending next week’s Corporate Jet Investor Malta Conference in St Julian’s, from 8-10 June. The focus of the conference is aircraft management, operations and charter.

Co-hosted with Transport Malta, the conference will build on the success of last year’s event, which attracted more than 200 attendees. With prevailing economic headwinds and conflict still raging across Eastern Europe and the Middle East, this year’s event will investigate the challenges and opportunities faced by aircraft management companies.

We look forward to seeing our industry friends and partners there.

Ionic Insights: Comparing the Business Jet Fleets of Saudi Arabia and the UAE

Welcome to Ionic Insights!

This, the latest in our series of detailed market analyses, compares the installed business jet fleets in both Saudi Arabia and the United Arab Emirates.

We assess the size, composition and age of both fleets, whilst simultaneously investigating the most popular OEMs and aircraft types.

The Business Jet Fleets in Saudi Arabia and the UAE

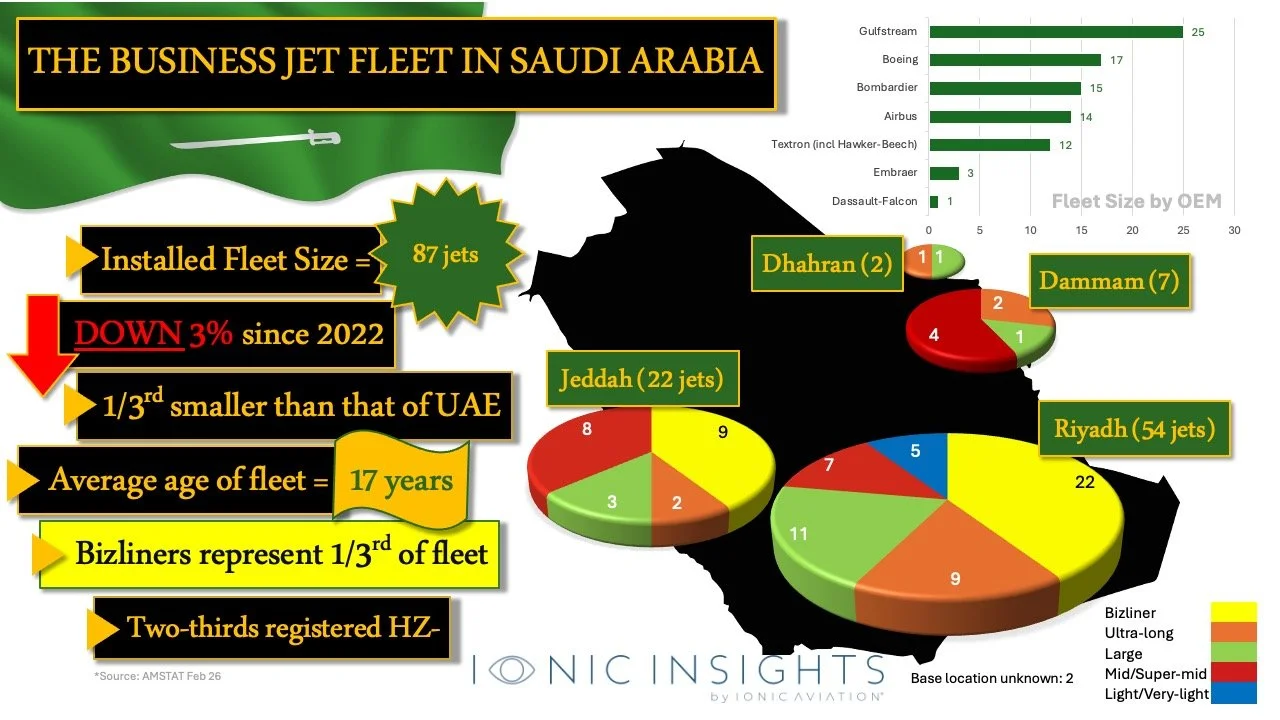

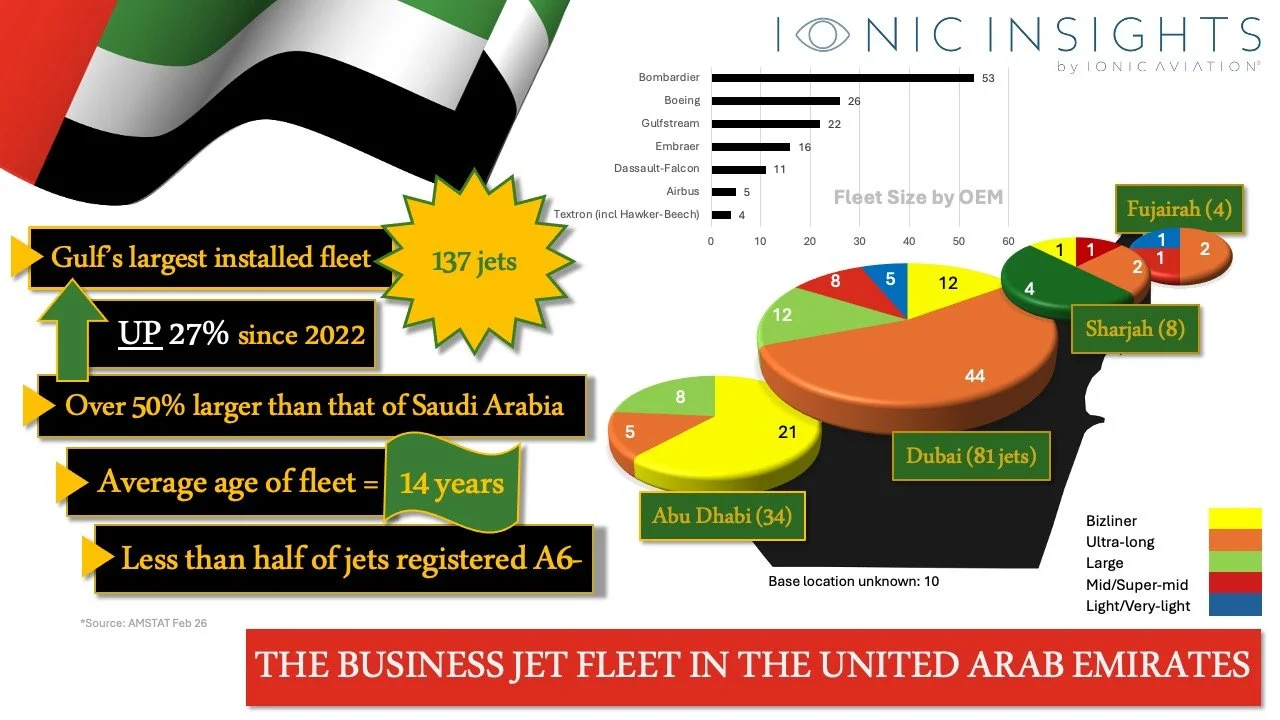

With a total of 137 aircraft the UAE boasts the region’s largest fleet. Having grown by 27% in four years, it is now over 50% larger than that of Saudi Arabia, which, with a fleet of 87 jets, has marginally reduced in size over the same period.

The reasons for the UAE’s rapid growth include the business friendly regime and attractiveness to the world’s wealthy and their aircraft.

The stagnation of the Saudi fleet can be traced back to the ‘Ritz-Carlton Crackdown’ where authorities detained hundreds of high-profile individuals as part of a 2017 anti-corruption drive. The reported seizure of over $100 billion in assets (including many aircraft) led to many Saudi elites moving assets overseas (including Dubai) whilst simultaneously developing an enthusiasm for non-scheduled services and the use of private terminals (FBOs). As such, there was a visible shift away from full ownership towards flexible aircraft usage via jet cards, charter and leasing.

Bombardier remains the largest OEM in the UAE, with the ultra-long-range Global (including the 5000, 6000 and 7500 variants) being particularly popular. In Saudi Arabia, Gulfstream continues to take top spot with its legacy G450 and G650/650ER models.

When it comes to aircraft registration, A6- registered aircraft account for less than fifty percent of all aircraft based in the UAE; whilst in Saudi Arabia two-thirds of all aircraft are registered domestically, HZ-.

Further information can be seen in the slides below:

The Business Jet Fleet in Saudi Arabia (Source: AMSTAT, Feb 26).

Substantial Bizliner Fleets

A common trend in both markets is the large number of corporate airliner/VVIP (‘bizliner’) aircraft in service. This popularity is most evident in Saudi Arabia where narrow and wide-body bizliners, from both Airbus and Boeing, make up over one-third of the total fleet.

The Business Jet Fleet in the UAE (Source: AMSTAT, Feb 26).

Market Outlook

Despite the current challenges, the long-term outlook for business aviation in Saudi Arabia and the UAE remains strong.

Significant and ongoing investment in infrastructure including the expansion of airports, FBOs and MRO facilities, combined with the recognition of aviation as a strategic enabler of economic growth bodes well for the future.

In Saudi specifically, strategic initiatives such as Vision 2030 (the strategic diversification away from oil), a $100 billion aviation investment programme, and the opening of the domestic charter market to foreign operators continue to lay the groundwork for growth and expansion across both the business and commercial aviation sectors.

We hope that the region returns to normality again soon.

Ionic Insights: Die Geschäftsreiseflugzeug-Flotte in Deutschland

Welcome to the latest edition of Ionic Insights.

This, the latest in our series of aircraft market analyses, focusses on the installed business jet fleet in Germany. We investigate the size, composition and age of the installed fleet, whilst simultaneously investigating the most popular OEMs and aircraft types.

Background and Economy

Germany is a large and diverse country in the heart of Western/Central Europe.

Consisting of sixteen federated states, it has a population of over 83 million and, in spite of a number of challenges — not least high energy costs, an aging population and skilled labour shortages — remains Europe’s largest (and the world’s third-largest) economy. Its key manufacturing sectors include machinery, automotive and chemical exports; whilst its modern service sector today accounts for over seventy-percent of GDP.

The Business Jet Fleet

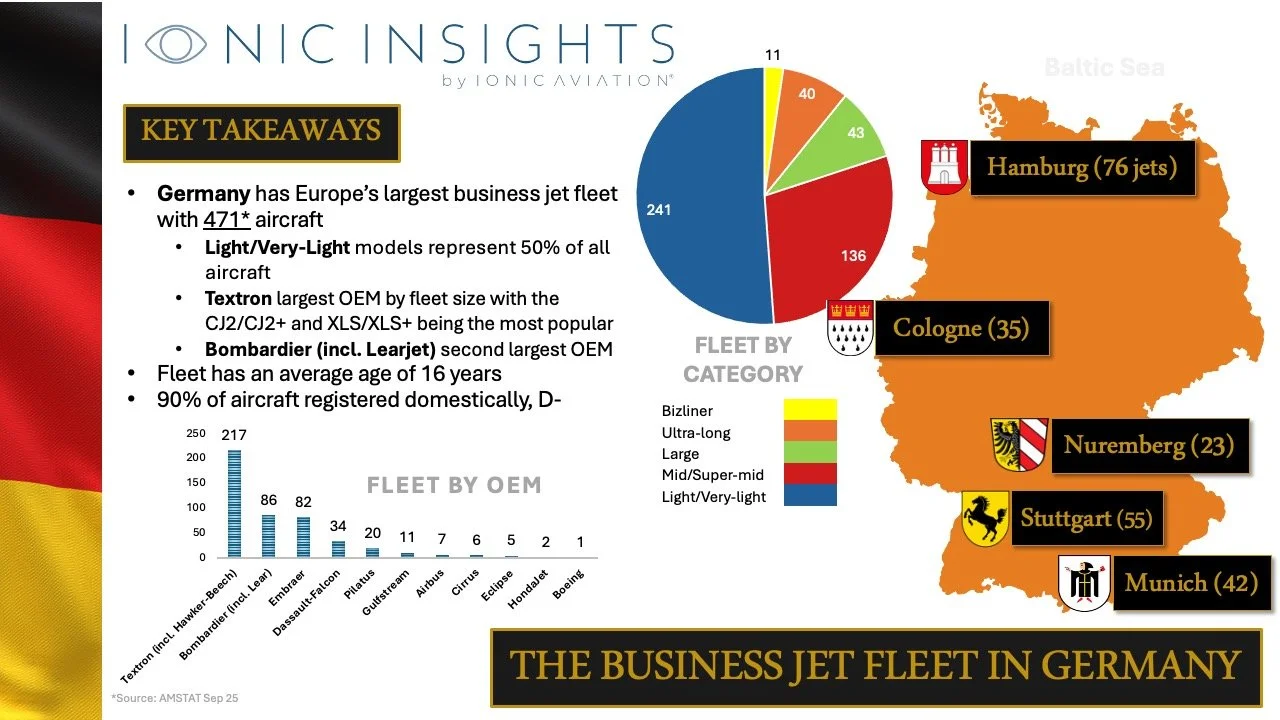

Germany boasts Europe’s largest installed business jet fleet of 471 aircraft. It is a large user of business jets for private and corporate travel, and benefits from a comprehensive network of airports and associated infrastructure.

Given Germany’s position at the geographical heart of Europe, it is of no surprise that half of all jets are of the Light/Very-light category and that Textron (including not only Cessna but Hawker-Beechcraft products also) makes up fifty-percent of the fleet. The most popular models are the Cessna CJ2/CJ2+ and Citation XLS/XLS+ — aircraft that are more than capable of carrying passengers across Europe from Germany’s central location.

Unlike the next largest European markets of the United Kingdom and France, where the bulk of jets are based in and around the metropolitan areas of London and Paris respectively, Germany’s fleet is dispersed widely in and around the country’s state capitals; with the second-largest city of Hamburg, not the capital Berlin, being home to the greatest number of aircraft (see the slide below).

Approximately ninety percent of all aircraft are registered domestically (D-); whilst the average age of the fleet is sixteen years.

Market Outlook

Despite some recent market volatility, Germany continues to lead Europe in jet charter, thereby driving new aircraft acquisitions by operators responding to HNW and corporate demand.

Aircraft ownership aside, the increasing popularity of charter, jet cards and fractional-ownership models is lowering barriers to entry and widening the customer base. And whilst the impact of regulatory cost pressures, including luxury taxes and environmental measures (such as carbon pricing, sustainable fuel mandates etc) increase operating costs and adversely impact demand, newer, more efficient aircraft (including the aforementioned entry-level Light and Very-light jets) are attracting a generation of new buyers and operators.

Given the above, and with full consideration of the economic, geopolitical and regulatory headwinds, we should, over the next decade, expect steady but by no means stellar growth in Germany’s business jet fleet, with the opportunities for aircraft financing increasing proportionately also.

Ionic Insights: Die Geschäftsreiseflugzeug-Flotte in Deutschland.

Ionic Insights: The Business Jet Fleet in Lapland

Welcome to our seasonal edition of Ionic Insights in which we focus on the installed business jet fleet in Lapland!

Lapland is Finland's northernmost region and makes up about one-third of the country’s overall landmass. The indigenous ‘Sámi’ people have lived in Lapland for centuries – their traditional homeland of Sápmi extending not only to Finland but across Sweden, Norway and Russia also. Lapland’s population, totalling approximately 180,000, is nowadays outnumbered by reindeer…

But, the importance of reindeer doesn't end there. The capital, Rovaniemi, is Lapland's largest city and is known as the official hometown of Santa Claus. Largely destroyed during World War II, Rovaniemi's post-war reconstruction centred around a street plan designed to resemble a reindeer, with roads forming the outline of the head and a stadium serving as the eye.

Lapland's GDP is greater than 7 billion euros, the majority of which is exported. The GDP per capita exceeds €40,000. Most of the gold used in Finnish coins is mined in Lapland, whilst the origin of the chocolate remains something of a mystery...

Lapland's economy is service sector driven, although industry (notably mining, metals and wood processing) and high-tech manufacturing remains important. The region boasts a burgeoning tourism sector and abundant natural resources such as timber and fresh water.

So, what of the business jet fleet in Lapland? The results of our throughly exhaustive year-end research can be found below... 👇

Ionic Insights: The Business Jet Fleet in Lapland.

Ionic Insights: The Business Jet Fleet in Poland

This, the latest in our series of detailed aviation market insights, focusses on the installed business jet fleet in Poland. We analyse the size, composition and age of the installed fleet, whilst simultaneously investigating the most popular OEMs, operators and aircraft types.

Economy

Home to a population of over 36 million and being the fifth largest country in the European Union by land mass, Poland’s GDP exceeds $300 billion and accounts for some 4.4% of the block’s total output.

Poland's economy is dominated by services, manufacturing and agriculture. Services account for over 50% of all activity and include the fast-growing tourism and technology sectors. Industry accounts for over one-third of GDP, with the production of automotive, machinery and domestic products, chemicals and furniture being particularly prevalent. Agriculture also remains important; the country is a significant exporter of a range of food products including apples, potatoes, beets and rye.

The Business Aircraft Fleet

Poland has a relatively small installed business jet fleet of 59 aircraft. The fleet is young with an average age of only 11 years.

Light/Very Light and Midsize/Super-midsize categories dominate; whilst Textron (Cessna/Hawker-Beechcraft) and Bombardier are the largest OEMs by fleet size, with 27% and 25% of the fleet respectively. The Cirrus Vision SF50, Hawker 400XP, Challenger 300/350/3500 and Pilatus PC-24 models are particularly popular.

93% of aircraft are registered domestically (SP-); whilst almost three quarters of all aircraft are based in and around the capital city of Warsaw.

The largest aircraft operators are Jet Story and AMC.

Market Outlook

Poland’s growth into a modern services-driven economy, combined with the continued expansion of its ICT and defence sectors will lead to a steady growth in aircraft ownership. A new generation of technology companies and entrepreneurs will drive the transition from ownership of Light, Midsize and Super-midsize jets to larger and more range-capable aircraft types. It is fair to assume that the availability of affordable financing will grow in parallel.

Albeit small at present, recent market activity would suggest that Poland is - in the opinion of Ionic Aviation - a market to watch.

Source: AMSTAT, Sep 25.

Ionic Insights: The Business Jet Fleet in East Africa

Welcome to the latest edition of Ionic Insights!

In advance of next week’s Aviation Africa Summit & Exhibition in Kigali, this, the latest in our series of detailed market insights, focusses on the size and scope of the installed business jet fleet in East Africa, more specifically the nations making up the East African Community.

We analyse the size, composition and age of the installed fleet, whilst simultaneously investigating the most popular OEMs and aircraft types.

Background

The East African Community (‘EAC’) is a regional organisation consisting of eight partner countries including Burundi, Democratic Republic of Congo, Kenya, Rwanda, Somalia, South Sudan, Tanzania and Uganda.

Home to over 330 million citizens, with a total land mass of over five million square kilometres and a combined GDP exceeding $300 billion the EAC was formed to deepen ties amongst member states. The principal areas of co-operation include: formation of a customs union, a common market, and ultimately political and monetary union.

Fleet

As it stands, the countries of the EAC have a small, combined business jet fleet of only 23 aircraft. This fleet pales in comparison to the fleets of Africa’s largest markets including South Africa (129 aircraft) and Nigeria (92).

Kenya is home to over half of all aircraft (13), whilst Burundi, Rwanda, Somalia, South Sudan have no business jet aircraft whatsover.

Midsize/Super-midsize aircraft models dominate, whilst Textron (Cessna/Hawker-Beechcraft) is the largest OEM by fleet size — the Citation Bravo and Sovereign models being particularly popular.

The fleet has an average age of over 27 years - almost twice that of the fleet in China (see our recent analysis).

Market Outlook

Despite past predictions and the ambitious, long-term potential of the EAC, significant fleet growth in countries other than Kenya is likely to be limited — with demand unlikely to extend beyond the light turboprops and helicopters which at present dominate the tourism sectors in countries including Tanzania and Uganda.

Ongoing infrastructure challenges, including pilot and engineer shortages; scarcity of fixed-base operators (FBOs), aircraft management companies and maintenance, repair and overhaul (MRO) services; regulatory concerns; complex permit regimes; inadequate airport infrastructure; and inflated ground handling and fuel costs, taxes, landing fees and navigation charges will continue to impact upon growth.

Finally, geopolitical, jurisdictional, operational, compliance and security risks, such as those resulting from conflict and opaque credit histories will unfortunately continue to impact upon the access to aircraft finance, thereby hampering significant fleet expansion in the region.

Source: AMSTAT, August 2025.

Ionic Insights: The Business Jet Fleet in China

Welcome to the latest edition of Ionic Insights!

This edition focusses on the size and scope of the business jet fleet in Asia’s largest market: China. We analyse the size, composition and age of the installed fleet, whilst simultaneously investigating the most popular OEMs, aircraft types and registries.

Fleet

China boasts a sizeable installed fleet of 204* business jet aircraft, and despite undergoing a recent period of contraction remains Asia-Pacific’s largest market.

The base locations of the fleet reflects the international nature of China’s business and ultra-high-net-worth (UHNW) communities. One-third of the fleet is based in the capital city of Beijing, whilst the vast majority of all aircraft are geographically biased towards the other more populous cities and regions along the eastern and southern seaboards; thereby enabling larger, range capable aircraft access to the wider APAC region and Pacific coast of the United States.

Gulfstream is the largest manufacturer (singlehandedly representing 40% of the overall fleet) with the G650/G650ER and G550 being the most popular models.

The fleet remains relatively young with a mean age of only 14 years.

The overwhelming majority of the fleet is registered domestically (B-), whilst a handful are registered in the United States (N), Aruba (P4-) and the Cayman Islands (VP-C) amongst others.

Market Outlook

Despite recent challenges, the long-term outlook for business aviation in China is positive.

The appetite for large-cabin aircraft, combined with the relatively youthful average fleet age, and the presence of a well-developed network of independent, third-party management companies enhances levels of comfort for lenders and lessors.

The Civil Aviation Administration of China (“CAAC”) projects that by 2043 China will become the world's largest aviation services market, with its current market value trebling to >$60 billion. This growth is expected to be fuelled by fleet expansion, greater airport capacity and the resultant increased demand for aviation services.

A summary of our analysis can be found in the slide below:

Source: AMSTAT, May 2024.

Ionic Finances New Gulfstream G280

Ionic Aviation is delighted to announce that it has successfully arranged the permanent financing of a new-delivery Gulfstream G280 aircraft for a client in Asia.

The project is testament to our track record of originating, structuring and successfully financing aircraft in diverse, developing markets and of our unrivalled global network across the international business and commercial aviation sectors.

Ionic would like to thank our client for their trust and our partners for their unwavering support.

Ionic MD Elected to Aviation Club Board

Ionic Aviation is proud to announce that our Managing Director, Graeme Shanks, has been elected to join the Committee of The Aviation Club UK. Having first joined the Club in 2007, Graeme is thrilled to have won the support and confidence of his industry peers, and is looking forward to playing an active part in the continued success of the Club and its membership.

The Aviation Club was founded in 1990 as a networking forum and vehicle for promoting the development and growth of all aspects of civil aviation. The Club boasts over 350 members from a broad cross-section of the civil aviation community, its membership drawn from airlines, banks, lessors, financiers, OEMs, regulatory bodies, the media and a wide range of other service providers.

Membership of the Club is open to all individuals with a professional interest in the civil aviation industry. Those interested in joining can do so by visiting The Aviation Club website.