Ionic Insights: Comparing the Business Jet Fleets of Saudi Arabia and the UAE

Welcome to Ionic Insights!

This, the latest in our series of detailed market analyses, compares the installed business jet fleets in both Saudi Arabia and the United Arab Emirates.

We assess the size, composition and age of both fleets, whilst simultaneously investigating the most popular OEMs and aircraft types.

The Business Jet Fleets in Saudi Arabia and the UAE

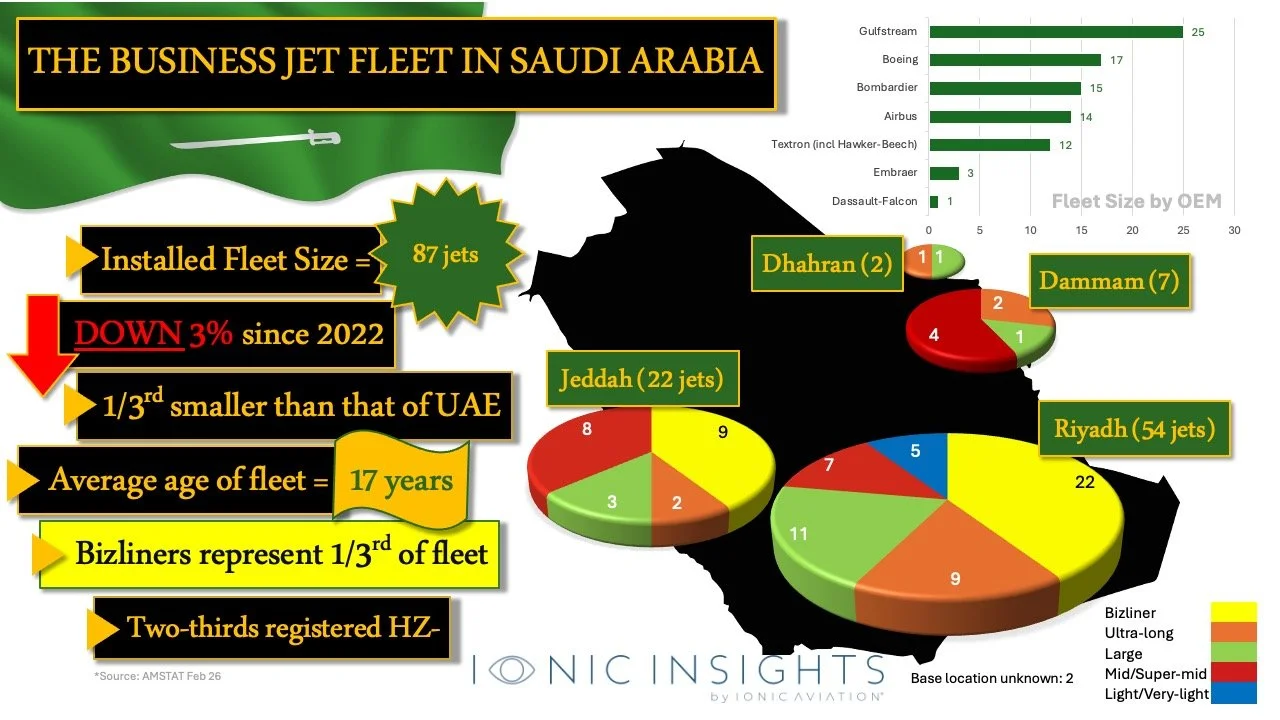

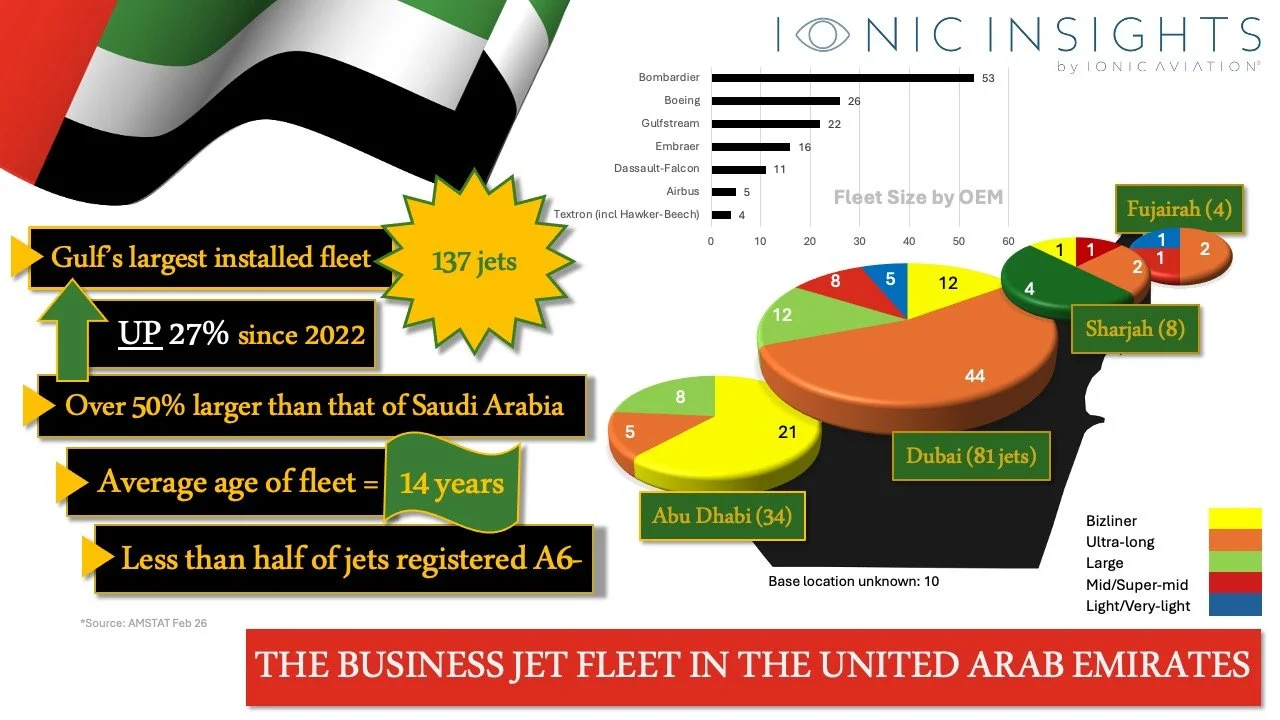

With a total of 137 aircraft the UAE boasts the region’s largest fleet. Having grown by 27% in four years, it is now over 50% larger than that of Saudi Arabia, which, with a fleet of 87 jets, has marginally reduced in size over the same period.

The reasons for the UAE’s rapid growth include the business friendly regime and attractiveness to the world’s wealthy and their aircraft.

The stagnation of the Saudi fleet can be traced back to the ‘Ritz-Carlton Crackdown’ where authorities detained hundreds of high-profile individuals as part of a 2017 anti-corruption drive. The reported seizure of over $100 billion in assets (including many aircraft) led to many Saudi elites moving assets overseas (including Dubai) whilst simultaneously developing an enthusiasm for non-scheduled services and the use of private terminals (FBOs). As such, there was a visible shift away from full ownership towards flexible aircraft usage via jet cards, charter and leasing.

Bombardier remains the largest OEM in the UAE, with the ultra-long-range Global (including the 5000, 6000 and 7500 variants) being particularly popular. In Saudi Arabia, Gulfstream continues to take top spot with its legacy G450 and G650/650ER models.

When it comes to aircraft registration, A6- registered aircraft account for less than fifty percent of all aircraft based in the UAE; whilst in Saudi Arabia two-thirds of all aircraft are registered domestically, HZ-.

Further information can be seen in the slides below:

The Business Jet Fleet in Saudi Arabia (Source: AMSTAT, Feb 26).

Substantial Bizliner Fleets

A common trend in both markets is the large number of corporate airliner/VVIP (‘bizliner’) aircraft in service. This popularity is most evident in Saudi Arabia where narrow and wide-body bizliners, from both Airbus and Boeing, make up over one-third of the total fleet.

The Business Jet Fleet in the UAE (Source: AMSTAT, Feb 26).

Market Outlook

Despite the current challenges, the long-term outlook for business aviation in Saudi Arabia and the UAE remains strong.

Significant and ongoing investment in infrastructure including the expansion of airports, FBOs and MRO facilities, combined with the recognition of aviation as a strategic enabler of economic growth bodes well for the future.

In Saudi specifically, strategic initiatives such as Vision 2030 (the strategic diversification away from oil), a $100 billion aviation investment programme, and the opening of the domestic charter market to foreign operators continue to lay the groundwork for growth and expansion across both the business and commercial aviation sectors.

We hope that the region returns to normality again soon.