Ionic Insights: Die Geschäftsreiseflugzeug-Flotte in Deutschland

Welcome to the latest edition of Ionic Insights.

This, the latest in our series of aircraft market analyses, focusses on the installed business jet fleet in Germany. We investigate the size, composition and age of the installed fleet, whilst simultaneously investigating the most popular OEMs and aircraft types.

Background and Economy

Germany is a large and diverse country in the heart of Western/Central Europe.

Consisting of sixteen federated states, it has a population of over 83 million and, in spite of a number of challenges — not least high energy costs, an aging population and skilled labour shortages — remains Europe’s largest (and the world’s third-largest) economy. Its key manufacturing sectors include machinery, automotive and chemical exports; whilst its modern service sector today accounts for over seventy-percent of GDP.

The Business Jet Fleet

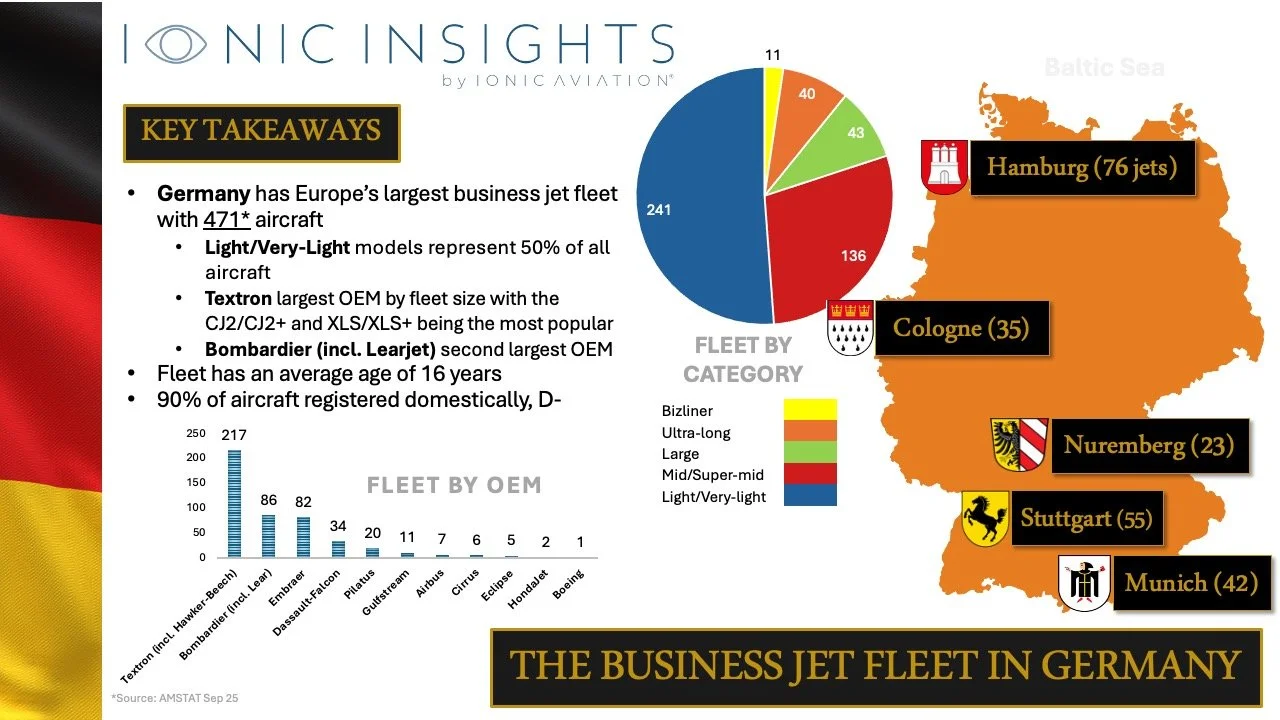

Germany boasts Europe’s largest installed business jet fleet of 471 aircraft. It is a large user of business jets for private and corporate travel, and benefits from a comprehensive network of airports and associated infrastructure.

Given Germany’s position at the geographical heart of Europe, it is of no surprise that half of all jets are of the Light/Very-light category and that Textron (including not only Cessna but Hawker-Beechcraft products also) makes up fifty-percent of the fleet. The most popular models are the Cessna CJ2/CJ2+ and Citation XLS/XLS+ — aircraft that are more than capable of carrying passengers across Europe from Germany’s central location.

Unlike the next largest European markets of the United Kingdom and France, where the bulk of jets are based in and around the metropolitan areas of London and Paris respectively, Germany’s fleet is dispersed widely in and around the country’s state capitals; with the second-largest city of Hamburg, not the capital Berlin, being home to the greatest number of aircraft (see the slide below).

Approximately ninety percent of all aircraft are registered domestically (D-); whilst the average age of the fleet is sixteen years.

Market Outlook

Despite some recent market volatility, Germany continues to lead Europe in jet charter, thereby driving new aircraft acquisitions by operators responding to HNW and corporate demand.

Aircraft ownership aside, the increasing popularity of charter, jet cards and fractional-ownership models is lowering barriers to entry and widening the customer base. And whilst the impact of regulatory cost pressures, including luxury taxes and environmental measures (such as carbon pricing, sustainable fuel mandates etc) increase operating costs and adversely impact demand, newer, more efficient aircraft (including the aforementioned entry-level Light and Very-light jets) are attracting a generation of new buyers and operators.

Given the above, and with full consideration of the economic, geopolitical and regulatory headwinds, we should, over the next decade, expect steady but by no means stellar growth in Germany’s business jet fleet, with the opportunities for aircraft financing increasing proportionately also.

Ionic Insights: Die Geschäftsreiseflugzeug-Flotte in Deutschland.